Top 15 Business Credit Cards For Poor Credit History In UK

Last Updated on

Securing a business credit card when you have a poor credit history can be challenging, but it’s not impossible. The right card can help you manage your business finances effectively while also rebuilding your credit score. In this guide, I will introduce you to 15 business credit cards available in the UK that are tailored for businesses with poor credit.

What Are Business Credit Cards for Poor Credit?

Business credit cards for poor credit are specifically designed to cater to individuals or businesses with lower credit scores. These cards typically have more lenient approval criteria, though they often come with higher interest rates and fees to mitigate the risk for the issuer.

- Differences from Regular Business Credit Cards: Business credit cards for poor credit may offer lower credit limits and fewer perks compared to regular cards.

- Benefits: These cards can be instrumental in helping rebuild your credit history if used responsibly.

- Drawbacks: The higher interest rates and fees can make these cards costly if balances are not paid in full each month.

How to Choose the Right Business Credit Card for Poor Credit?

What Should You Look For in a Business Credit Card?

When selecting a business credit card for poor credit, it’s crucial to consider the following factors:

- Interest Rates: Higher than average rates are common; aim for the lowest rate possible given your credit situation.

- Fees: Look out for annual fees, late payment fees, and other charges.

- Credit Limits: Cards for poor credit often have lower limits, so ensure it meets your business needs.

- Rewards: Some cards still offer rewards; however, prioritize rebuilding credit over rewards.

Secured vs. Unsecured Business Credit Cards: Which is Better?

- Secured Cards: Require a deposit which acts as your credit limit. They are easier to get approved for and are a good option for rebuilding credit.

- Unsecured Cards: Do not require a deposit, but typically come with higher interest rates and fees.

How Does a Business Credit Card Help Improve Poor Credit?

Using a business credit card responsibly—by paying off your balance in full each month and keeping your credit utilization low—can significantly improve your credit score over time.

Top 15 Business Credit Cards for Poor Credit in the UK With Bad Credit History

1. Capital on Tap Business Card

- APR: 29.9%

- Features:

- No annual fee.

- Cashback on business purchases.

- Credit limit up to £50,000.

- Additional cards for employees at no extra cost.

- Easy online account management.

- Advantages:

- High credit limit, even for businesses with bad credit.

- Cashback rewards can help offset costs.

- No annual fee keeps it affordable.

- Disadvantages:

- The APR is quite high, making it expensive if you don’t pay off the balance monthly.

- Requires an established business with a minimum revenue.

2. Aqua Business Credit Card

- APR: 34.9%

- Features:

- Focuses on helping build credit, with alerts to track improvements.

- Low initial credit limit.

- Free eligibility checker without impacting your credit score.

- Advantages:

- Specifically designed for businesses with poor credit.

- Credit-building tools and alerts are beneficial.

- Easier approval process for those with low credit scores.

- Disadvantages:

- The low credit limit might not suffice for larger business needs.

- The high interest rate can make it costly if you carry a balance.

3. Barclaycard Business Card

- APR: 26.9%

- Features:

- Up to 56 days of interest-free purchases.

- No annual fee for the first year (then £32 annually).

- Online tools for managing accounts and tracking expenses.

- Advantages:

- Offers a generous interest-free period.

- No annual fee in the first year reduces initial costs.

- Helpful online tools for expense management.

- Disadvantages:

- The APR rises significantly after the interest-free period ends.

- Approval may be harder for those with very poor credit.

4. Vanquis Bank Business Card

- APR: 39.9%

- Features:

- Specifically aimed at those with poor credit.

- Starts with a low credit limit, which can increase over time.

- Mobile app for easy account management.

- Advantages:

- High acceptance rate for applicants with bad credit.

- Good option for rebuilding credit with careful use.

- Disadvantages:

- Very high APR, so carrying a balance can be expensive.

- The low initial credit limit may limit its usefulness for some businesses.

5. Tide Expense Card

- APR: 30.3%

- Features:

- No monthly fees or hidden costs.

- Real-time notifications for transactions.

- Integrates with popular accounting software.

- Advantages:

- No monthly fees, making it budget-friendly.

- Instant transaction alerts aid in better financial control.

- Disadvantages:

- It’s not a traditional credit card; more of a prepaid expense card.

- Requires a business account with Tide to use.

6. Think Business Loan Credit Card

- APR: 35.9%

- Features:

- Designed for businesses with poor credit.

- Fast and easy approval process.

- Flexible credit limits based on business needs.

- Advantages:

- Tailored for businesses with a history of poor credit.

- Quick approval, providing swift access to funds.

- Disadvantages:

- High interest rate, making it costly if balances aren’t managed well.

- Limited additional benefits or rewards compared to other cards.

7. Cashplus Business Credit Card

- APR: 29.9%

- Features:

- Approval doesn’t require a credit check.

- Option to use as a prepaid card for better budgeting.

- Ideal for small businesses with minimal spending needs.

- Advantages:

- Accessible to businesses with poor credit since no credit check is required.

- Prepaid option helps avoid debt and manage spending.

- Disadvantages:

- It’s not a traditional credit card, so it won’t help build credit.

- Lacks many features compared to other business credit cards.

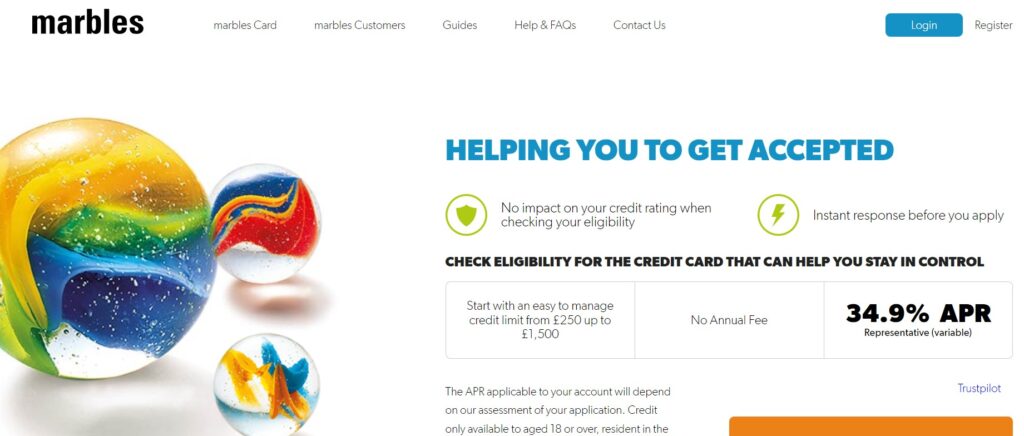

8. Marbles Business Credit Card

- APR: 33.9%

- Features:

- Quick eligibility check without affecting your credit score.

- Manageable credit limits that help control spending.

- No annual fee, making it cost-effective.

- Advantages:

- No annual fee helps keep overall costs low.

- Useful for credit building if used responsibly.

- Disadvantages:

- High APR means carrying a balance could be expensive.

- Basic features with limited perks or rewards.

9. NewDay Business Card

- APR: 34.0%

- Features:

- Regular credit limit reviews based on usage.

- Online account management for easier expense control.

- Contactless payments for added convenience.

- Advantages:

- Regular reviews may lead to higher credit limits over time.

- Convenient online management.

- Disadvantages:

- High interest rate, making it costly if balances are not paid in full.

- Low initial credit limit could be restrictive.

10. Lloyds Business Credit Card

- APR: 27.9%

- Features:

- Introductory low interest rate on purchases for the first few months.

- Rewards for business spending, like cashback or points.

- Manageable fees with straightforward terms.

- Advantages:

- Introductory low rate helps manage early business expenses.

- Rewards program adds value to business spending.

- Disadvantages:

- APR increases after the introductory period ends.

- Approval might be harder for businesses with very poor credit.

11. American Express Business Card

- APR: 25.9%

- Features:

- Flexible payment options, including the ability to carry a balance.

- Earn rewards points on all spending, redeemable for travel, gift cards, and more.

- Includes travel perks such as airport lounge access.

- Advantages:

- Attractive rewards program, particularly for frequent travelers.

- Flexible payment options to suit your business needs.

- Disadvantages:

- Higher APR, so it’s best for those who can pay off their balance monthly.

- Limited acceptance in the UK compared to Visa and Mastercard.

12. Santander Business Credit Card

- APR: 29.9%

- Features:

- Fixed low interest rate for the first 12 months.

- No annual fee, which keeps overall costs down.

- Simple online and mobile banking tools for managing finances.

- Advantages:

- Initial fixed low rate is ideal for managing early expenses.

- No annual fee reduces ongoing costs.

- Disadvantages:

- The interest rate increases after the first year.

- Strict approval criteria may limit accessibility for those with poor credit.

13. TSB Business Credit Card

- APR: 28.9%

- Features:

- Up to 25 days interest-free on purchases, offering flexibility for payments.

- Rewards on spending, including cashback and discounts on business expenses.

- Online tools for easy tracking of business expenses.

- Advantages:

- Interest-free period provides flexibility in managing cash flow.

- Rewards program offers cashback and discounts.

- Disadvantages:

- Interest-free period requires full repayment to avoid charges.

- Higher APR after the introductory period ends.

14. Sainsbury’s Bank Business Card

- APR: 27.0%

- Features:

- Earn Nectar points on all purchases, redeemable at Sainsbury’s and other partners.

- Manageable credit limit tailored to small businesses.

- Competitive APR, especially for businesses with moderate credit.

- Advantages:

- Nectar points program adds value to everyday spending.

- Reasonable APR compared to other cards for poor credit.

- Disadvantages:

- Strict approval criteria may limit access for those with poor credit.

- Limited credit limit for new businesses or those with very poor credit.

15. Tesco Bank Business Credit Card

- APR: 29.9%

- Features:

- Earn Clubcard points on all spending, redeemable for Tesco vouchers or other rewards.

- No foreign transaction fees, ideal for businesses that operate internationally.

- Flexible credit limits based on business needs.

- Advantages:

- Clubcard points program adds value to your spending.

- No foreign transaction fees save money on international purchases.

- Disadvantages:

- High APR, so carrying a balance can be expensive.

- Limited credit limit for businesses with poor credit histories.

What Are the Alternatives to Business Credit Cards for Poor Credit?

Secured Loans

Secured loans require collateral, which lowers the risk for the lender and increases your chances of approval even with poor credit. These loans often come with lower interest rates or zero interest rates compared to unsecured loans or credit cards.

Merchant Cash Advances

This option involves borrowing against your future sales. It’s quick and easy to obtain but comes with high fees and should be considered carefully.

Credit Builder Loans

These loans are specifically designed to help you build or rebuild your credit. The lender holds the loan amount in a secured account while you make payments, helping you to build credit.

Conclusion

Selecting the right business credit card is crucial, especially when you have a poor credit history. By choosing from these top 15 options and using the card responsibly, you can work towards rebuilding your credit and ensuring the financial health of your business. Remember, the key to improving your credit score is consistency and careful management of your finances. Also, you can check the best card payment machines for small business in UK and pick the best.

Frequently Asked Questions (FAQs)

1. Can I Get a Business Credit Card with a Bad Credit Score?

Yes, several credit cards are available for businesses with bad credit. These cards typically have higher interest rates and lower credit limits, but they can help you rebuild your credit if used responsibly.

2. How Long Does It Take to Improve My Business Credit Score?

Improving your business credit score can take several months to a few years, depending on your financial habits. Consistently paying on time and keeping your credit utilization low are key factors.

3. What Happens If I’m Denied a Business Credit Card?

If you’re denied a business credit card, consider alternative financing options like secured cards, credit builder loans, or secured business loans. You should also review the reasons for denial to improve your credit standing.